This is an age of disruption. Tech companies are some of the most relevant companies that will lead us into the next several decades. Hence, it is important to have some of the best tech companies within your investment portfolio. However, if you could only choose one, what is the best tech company to invest in?

I would invest in Microsoft. I believe it has the highest earnings visibility, is one of the strongest companies in the world today and is still selling at a reasonable valuation.

During the Grey Rhino Show in July 2020, I shared about Microsoft. It was selling at $214 then but the share price has gone up by 54% and is $330 today. This increase can be alluded to its earnings having increased substantially and its growth over the last 1.5 years. Although it might not be as attractive as 1.5 years ago, I think it is still the best tech company to invest in for the long haul.

In this article, I will look at 3 areas:

1. Microsoft’s business segments and growth projection

2. Microsoft’s valuation versus others

3. Microsoft’s ability to weather headwinds versus others

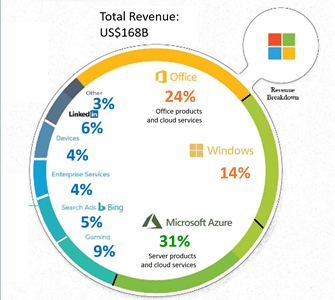

A breakdown of Microsoft’s 3 main business segments

1. Legacy business: Windows operating systems and Office Suites. These take up a third of the business.

2. Fast-growing cloud business: Microsoft Azure. This takes up another third of the business.

3. Smaller portfolios: Xbox, Bing, LinkedIn. These take up the last third of the business.

An analysis of Microsoft’s growth projection

Fast-growing cloud business: Microsoft Azure

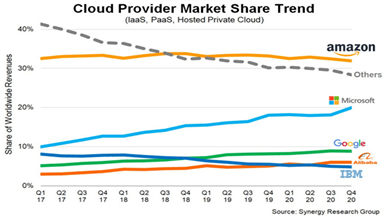

This cloud business is its crown jewel. It grew by 27% year on year from 2020 to 2021. The cloud industry has a lot of growth potential. International Data Corporation (IDC) forecasts that “whole cloud” spending will reach 1.3 trillion by 2025 and sustain a compound yearly growth rate of 16.9%. Additionally, taking a closer look at the cloud market, you will realise that even though the leader is still Amazon, which holds about 30% market share, it has been quite stable. Instead, 2 other companies have been growing their market share.

Microsoft has grown its market share from approximately 10% to 20% from 2017 to 2020. The other company with growing market share is Google. Other companies have been experiencing decline over the years. So, with the growth of the cloud industry and the gaining of market share by Microsoft Azure, I think a growth rate of more than 20% is likely to be sustained for the next 5 to 10 years.

Legacy business: Windows and Office Suites

In August 2021, Microsoft announced that in March 2022, it is going to hike the price of its office subscription, by between 9% to 25%. Hence, we are likely to see a jump in the earnings for this segment. However, beyond this, this segment will not be growing extremely fast as it is a relatively mature business. Microsoft also already has the lion’s share in the market. Hence, I think this segment will grow at somewhere between the high-teens and low double-digits.

Smaller portfolios: Xbox and LinkedIn

Between 2020-2021, the 2 segments that have been growing fast are Xbox and LinkedIn, but I will only focus on Xbox. The number of Xbox consoles that was shipped in 2020 was 3.3 million units. In 2021, it is expected to grow to 12 million units. And by 2025, it is expected to grow to 34 million units. This shows a big jump in Xbox consoles that are being shipped.

Xbox is also going to launch some important titles in 2021, bringing more avid gamers to its platform. Lastly, Xbox created GamePass, pioneering subscription-based gaming. Subscribing to Xbox will grant people access to Xbox’s suite of games. This makes it a very recurrent business, which is a very good business model.

Microsoft’s Enterprise business is also a dark horse. It currently only has a relatively small market share in a big market. Hence, if Microsoft can break into this space and become more dominant, this can also be a very fast-growing segment, growing at a mid-teens level.

An overview of Microsoft’s business segments

Piecing all 3 together, a growth of about 15% yearly for the next 5 to 10 years is highly likely. Hence, Microsoft’s earnings has a good visibility for the next 5 to 10 years.

A comparison of Microsoft’s valuation to others

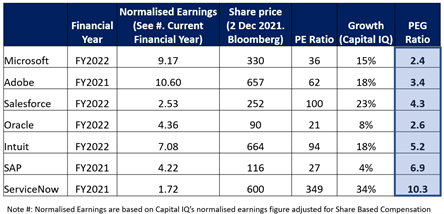

As a rule, I set a boundary of about 3x for price earnings growth (PEG) ratio. A PEG ratio beyond that is too expensive. And tech companies have had a big run-up in their share prices, especially at the later part of Covid-19. So, is it still at a good valuation to buy into?

I am looking at the most recent year and their normalised earnings at the 3rd column. What are normalised earnings? A company has GAAP earnings in its financial statements which follow the accounting standards. It also has its non-GAAP earnings. The non-GAAP earnings is usually what the management view as the company’s true earnings after taking away the non-cash and one-off items.

I will use non-GAAP earnings but with share-based compensation added back. Share-based compensation is a non-cash item but should be added back in as it is a cost to the shareholders. Hence, I think it is prudent to add back the share-based compensation to get the company’s true earnings.

For PEG ratio, I will use Capital IQ as a gauge and look at December 2nd 2021’s share price. Some companies have more than 3x PEG ratio. The only 2 that are within the 3x PEG ratio are Microsoft and Oracle. However, Oracle’s growth rate of 8% is too slow. I prefer a 10% to 20% growth rate. So, of these companies, Microsoft represents a good valuation.

However, there is a caveat. If you refer to my previous video. If interest rates were to go up, then Microsoft’s progress might be impeded – it might experience headwind.

A comparison of Microsoft’s ability to weather headwinds to others

Macroeconomic headwinds to the Big Tech companies includes the anti-trust, global minimum tax, and inflation and interest rates environment.

Microsoft and anti-trust concerns

In July 2020, US lawmakers summoned the chief of the Big Tech companies to enquire about their monopoly. However, Microsoft was not summoned because after its anti-trust issue in 1990s, it has been very careful to stay below the radar. Hence, I think Microsoft today has the least risk of anti-trust concerns.

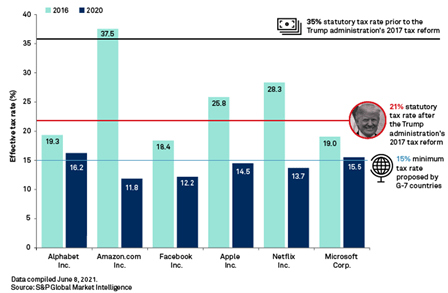

Microsoft and the global minimum tax

The G7 Nations have agreed to a global minimum tax of 15%. Hence, if certain countries are taxed lower than that, they might have to top up the difference. Looking at the latest earnings, only Alphabet (Google) and Microsoft’s current tax rate is above 15%. Thus, if this global minimum tax is introduced, it is unlikely that Microsoft will be affected.

Microsoft and the rate of inflation

Inflation is now rapidly increasing and this could lead to the faster increase of interest rates in 2021. We are seeing labour inflation, and hence companies who engage a lot of blue-collar workers, like Amazon, will be the most at risk. As interest rates, Microsoft will have a good runway ahead. So it is still a very safe company to own in the long haul. However, the ride will be bumpy because of the global macroeconomic environment.

Conclusion: Microsoft is THE tech company

After this analysis, it is no wonder that Microsoft is my choice if I can only choose a single tech company as a core part of my portfolio. If the macroeconomic conditions allow you to buy Microsoft shares at a lower price, you should take advantage of the opportunity too! With this, I wish you all prosperity in your investments.

Important notice

If you would like to seek advice on your personal investment portfolio, get in touch with me at heb@thegreyrhino.sg or 8221 1200, I would love to connect with you.

Stay updated with the latest news and insights, subscribe to my newsletter, and spread the word.